The Council of Canadian Academies released The State of Science, Technology, and Innovation in Canada, its 251-page flagship report last updated in 2018. It paints a gloomy, but familiar, picture of the Canadian economy: productivity and innovation keep dropping, and this is a decades-long trend, not a blip.

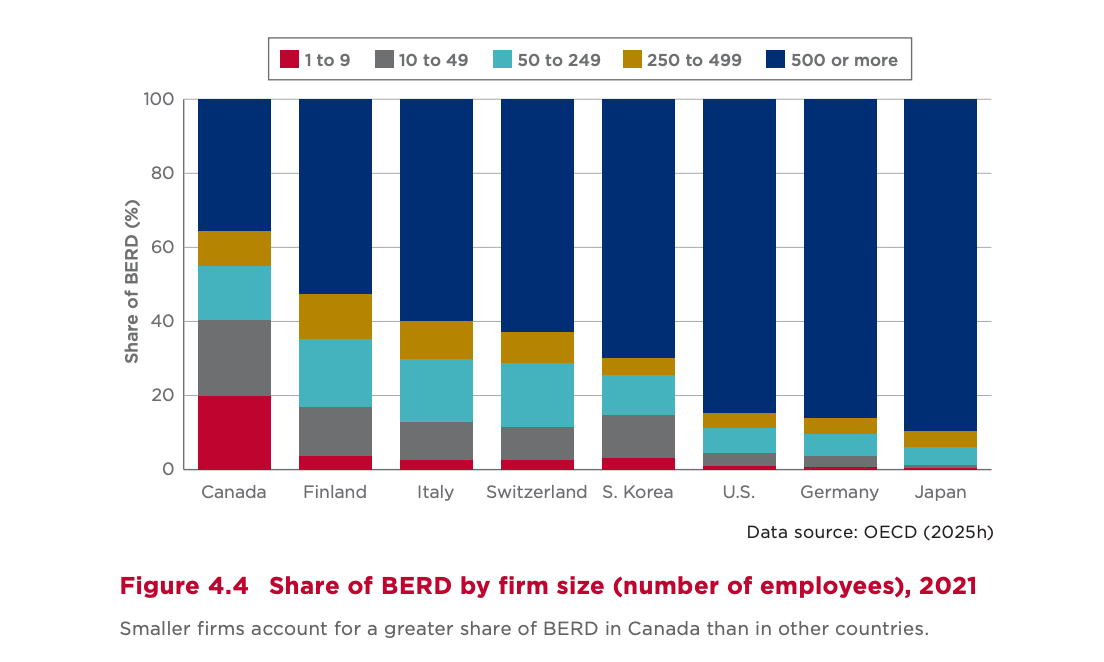

The above chart (page 78) shows business expenditures in research and development (BERD) broken out by firm size. The majority of R&D is being done by small firms, with only 36% of BERD by large enterprises (compared with 85% in the US). A self-fulfilling explanation is the relative lack of large firms in Canada.

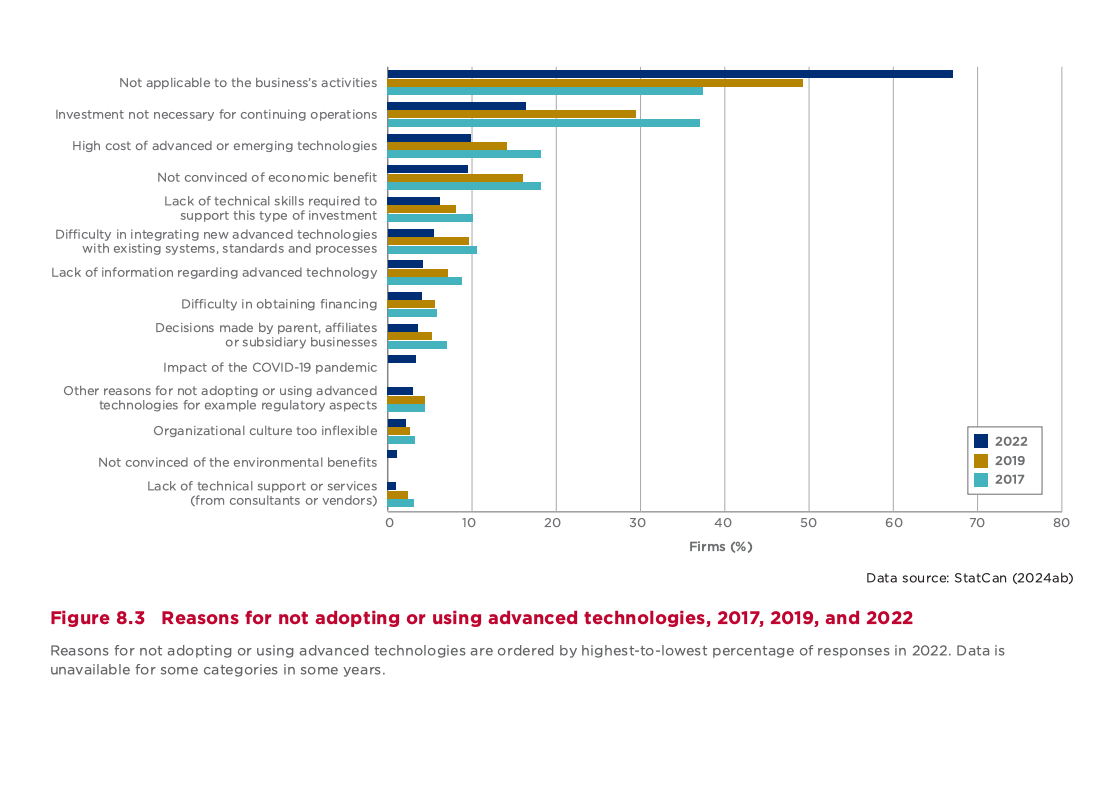

This chart (page 150) explains the snail's pace of technology adoption: the #1 reason for not adopting new technology, by a wide margin, was the feeling that it was “not applicable to the business's activities.”

This is not a good sign for rapid AI-adoption or rapidly doing anything in Canada. If business leaders think of innovation as “not applicable” then no amount of incentives will get them to move faster.

It reminds me of a conversation I had at Source Canada with a successful entrepreneur. He summarized the difference between selling to American vs Canadian corporations:

“The American buyer is looking at me as a source of competitive advantage, to get an edge over their rivals. They're rewarded for taking risks. In Canada it's the opposite. There's less competitive drive and they are penalized for risk-taking.”

Yet Another Buy Canadian Gap

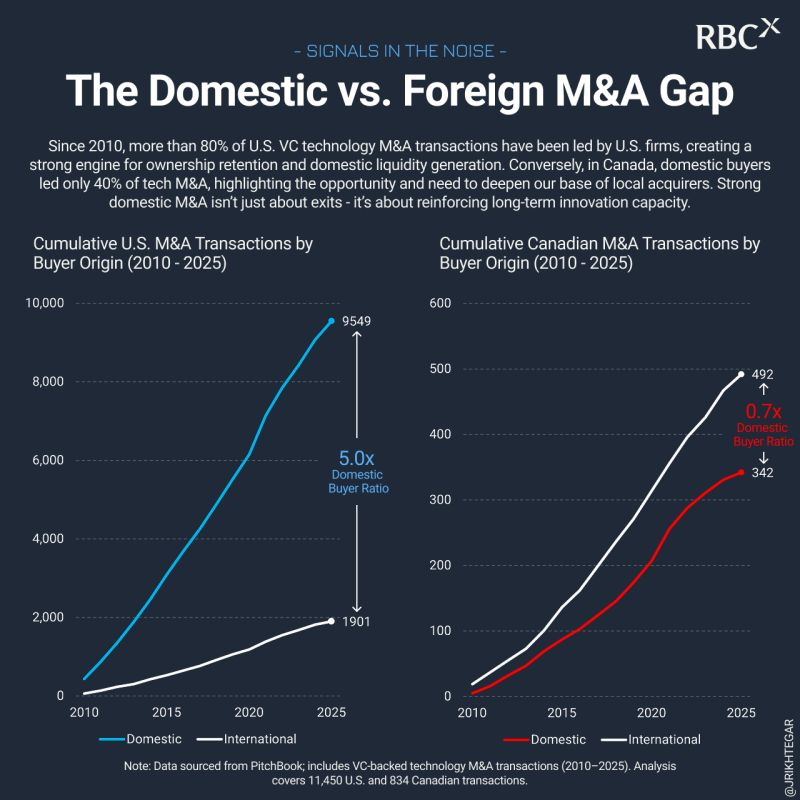

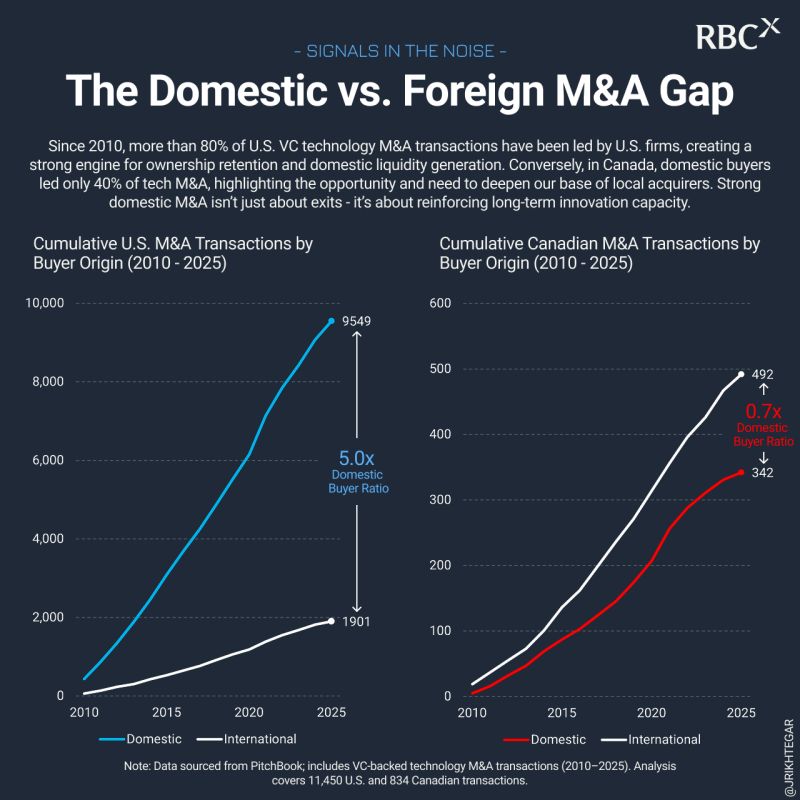

John Rikhtegar, from RBCx, posted this interesting comparison of who buys US vs Canadian startups. America buys 5X more US tech firms than they sell to international buyers. In Canada the radio is 0.7 (meaning foreign buyers buy more of our companies than we buy ourselves).

The advantages of Canadian firms acquiring Canadian startups is obvious: “When local firms acquire local companies, more of the long-term value - IP, talent, and reinvestment cycles - stays in-market. This is a foundational advantage of the U.S. ecosystem,” according to Rikhtegar.

Buy Ontario Please!

Ontario tabled its Buy Ontario Act, 2025 currently making its way through the legislature. The idea is to compel Ontario government organizations to prefer Ontario-based, then Canadian-based, firms over foreign entities.

This makes sense but, as one government organization told me, this is all performative unless there are additional funds to pay for switching costs, eg from a US-tech solution to a Canadian one. Not to mention funds to defend trade actions and lawsuits.

Buying Ontarian (and Canadian) is an essential boost of domestic vs foreign-owned technology firms. But there will be costs associated with finding, qualifying and switching to domestic firms.

If you have news, insights or tips about using procurement to drive innovation in Canada, just reply to this email or add a comment below.